I'm not sure that's a good idea anyhow. If your garage burns down, will your homeowner's (or other insurance) cover it at the value you placed with the collector car insurer?[U

"Did I mention that you can no longer "take your car off the road temporarily" and put a hold on insurance in MA?"

You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

What are you valuing your e9 for insurance purposes

- Thread starter scottevest

- Start date

I told my sons years ago " If you commit the worst crimes, I will still love you but if you burn down our house, I won't." So far so good.

When I’ve inquired about removing everything except fire and theft over the Winter, Hagerty went like “deer in the headlights”. Didn’t pursue it.

Scott, totally forgot when you began this process. What was the approximate time they took to finalize an agreed value for your E9? Reason being, when I first spoke to Hagerty, they had agreed values right away. Realistically, if you go in with a “unreasonable” number say for instance $250K, they might just have to think about. As a codicil, I came to the table with a total of 10 cars that needed coverage. Volume discount? Am presuming you will want to drive your car about 5K/year and have good storage facility to keep it safe and indoors.After much back-and-forth they finally agreed to the valuation although I suspect if anything were to happen, I would have a massive argument about the cost to repair. Going to look into Haggerty

Hugh

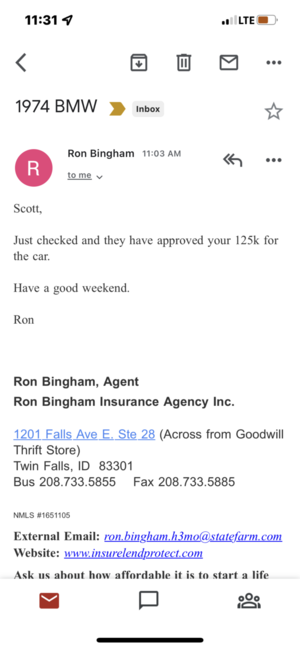

I requested on Feb 7th. Got this push back, but sent some comps from BAT. Hard to believe the car is worth $125k; more likely less depending upon the auction. But I have no intention of wrecking or selling it. I know it would cost me ~$100k to replace it, and then I wouldn't know if it was sorted. I didn't have to let them know milage. I suspect I will drive around 2-3k/year, unless I take a trip. I really don't drive that much, just a few miles a day to the trailhead since I work at home and have been really enjoying my Porsche 964.Scott, totally forgot when you began this process. What was the approximate time they took to finalize an agreed value for your E9? Reason being, when I first spoke to Hagerty, they had agreed values right away. Realistically, if you go in with a “unreasonable” number say for instance $250K, they might just have to think about. As a codicil, I came to the table with a total of 10 cars that needed coverage. Volume discount? Am presuming you will want to drive your car about 5K/year and have good storage facility to keep it safe and indoors.

Hugh

They are right, we went over this many times. A market price is not established by asking prices but rather by actual transactions that took place.I requested on Feb 7th. Got this push back, but sent some comps from BAT. Hard to believe the car is worth $125k; more likely less depending upon the auction. But I have no intention of wrecking or selling it. I know it would cost me ~$100k to replace it, and then I wouldn't know if it was sorted. I didn't have to let them know milage. I suspect I will drive around 2-3k/year, unless I take a trip. I really don't drive that much, just a few miles a day to the trailhead since I work at home and have been really enjoying my Porsche 964.View attachment 136473

I provided multiple comparable sales not asking prices.They are right, we went over this many times. A market price is not established by asking prices but rather by actual transactions that took place.

In that case you are right.I provided multiple comparable sales not asking prices.

How many states have "Excise Tax" for cars? In NY I never heard of it, in Ma, we gotta pay every year. This is one time I am happy that the RMV is dumb. Look at the assessed values that my excise taxes are based on. If you hate me, you'll let them know otherwise. What I also laugh at is the 40 cents..........................but then again, my son's english class grade is taken to three decimal points.

My M6 E9 E3

My M6 E9 E3

I will never forget my first BMW 320i in 1977. I got my excise tax bill but the town used the value of the 630CSi ! I think the bill was in the thousands. Myheart stopped

You're making me feel a little better about CA. The CA DMV is soooooo messed up.How many states have "Excise Tax" for cars? In NY I never heard of it, in Ma, we gotta pay every year.

thehackmechanic

Well-Known Member

Just to chime in here... if others have already said this, forgive me.

Whether it's Hagerty or one of the other collector car insurers, what you want is an "Agreed Value" policy. That is, you want a policy where you say "I want to insure my E9 for $120k" (or whatever your number is), they agree, quote you a price for that, you pay it, and then you have a contract that if the car is stolen or totaled, that's what they'll pay. $120k is a number that Hagerty would NOT agree to for an E9 until a few years ago when one of us wanted that value on his car, they said "we don't think the market supports that," he presented data (mostly numbers from BaT), and they acquiesced. But the point is that if you have a standard policy like you have for a daily driver, if the car gets hit/totaled, you really have very little protection. You can try to justify the value of the car, but they're not really under any legal obligation to pay you what you think it's worth because you haven't entered into a contract with them to pay an "agreed value."

Agreed value policies like the one I have with Hagerty typically have a few requirements:

I believe I currently have my E9 insured for $60k. It's very pretty, but not at the concours level of some of the other cars on this thread. But these days that's probably a bit low.

For all 9 cars (three 2002s, the Bavaria, the E9, the Euro '79 635CSi, the Z3 and M Coupe, and the '74 Lotus Europa Twin Cam Special), I pay an annual premium of about $1,050. Total. For all nine of them. Of course, I live in the safe confines of Newton MA, and I don't have high agreed values on most of the cars.

--Rob

Whether it's Hagerty or one of the other collector car insurers, what you want is an "Agreed Value" policy. That is, you want a policy where you say "I want to insure my E9 for $120k" (or whatever your number is), they agree, quote you a price for that, you pay it, and then you have a contract that if the car is stolen or totaled, that's what they'll pay. $120k is a number that Hagerty would NOT agree to for an E9 until a few years ago when one of us wanted that value on his car, they said "we don't think the market supports that," he presented data (mostly numbers from BaT), and they acquiesced. But the point is that if you have a standard policy like you have for a daily driver, if the car gets hit/totaled, you really have very little protection. You can try to justify the value of the car, but they're not really under any legal obligation to pay you what you think it's worth because you haven't entered into a contract with them to pay an "agreed value."

Agreed value policies like the one I have with Hagerty typically have a few requirements:

- You have to show that you and every other licensed driver in the house have another car on which you're listed as the primary driver, and that the car is fully insured. I believe that they leech liability off your other policy.

- You have to show that the car is kept in a locked garage (though I believe Hagerty has relaxed this).

- There is an annual mileage limit in the 2,000 to 3,000 mile range, but it's negotiable.

- But the main thing is that a collector car IS NOT A DAILY DRIVER. You can't use it as a daily. You can't commute to work in it. That's where the cars are at the greatest risk for accidents. You can drive it nights and weekends basically to your heart's content.

I believe I currently have my E9 insured for $60k. It's very pretty, but not at the concours level of some of the other cars on this thread. But these days that's probably a bit low.

For all 9 cars (three 2002s, the Bavaria, the E9, the Euro '79 635CSi, the Z3 and M Coupe, and the '74 Lotus Europa Twin Cam Special), I pay an annual premium of about $1,050. Total. For all nine of them. Of course, I live in the safe confines of Newton MA, and I don't have high agreed values on most of the cars.

--Rob

Last edited:

This is an interesting discussion. Everyone has their own comfort level with what they feel their car may be worth. Many of us are probably guessing low. But this is really about protecting yourself if you should lose your Coupe. In the event of a total loss, would $60K get you another like the one you just lost? I don't think so. So how far do you go? BAT has certainly defined the E9 Coupe as an appreciating Classic. In my world, I try to balance what I think I would need to get another Coupe, with what premium I am willing to pay. I mean, I don't drive it that much, but I certainly love it and would certainly have to replace it if something happened to it. Plus if you have other Classics, things get complicated. Helps to share these views so we can feel comfortable/protected as well as we can and still exercise our Classics

we got rid of what Georgia called ad valorem taxes on vehicles about 7 years ago. we renew license plates on your birthday. so it became know as the birthday tax. old cars always got off easy. but a 45000 car was routinely 700 bucks when it was a year old ... each year it would drop slightly ...

georgia used to not charge sales tax on vehicles sold by individuals ... so they had no way to track values. now they do, so they get the value that you pay.

i have found what Rob stated equals the experience that most of us have. my coupe is insured through Heacock ... right now it is under-insured since the work being done on the car isn't complete ... 50k to 60k (i forget the current amount). once all the work is complete, i will go through the motions to get the agreed value of the 2800cs upwards of 100k to 125k. face it insurance is a form of legalized gambling - you are buying it in case something unexpected happens. but when you need it, you want to be sure that its there. for those of us with 2800cs, it takes a little more work to get it insured for the right value. when i get to that discussion, i will be leveraging the best information i can find on comparable sales of 2800cs.

georgia used to not charge sales tax on vehicles sold by individuals ... so they had no way to track values. now they do, so they get the value that you pay.

i have found what Rob stated equals the experience that most of us have. my coupe is insured through Heacock ... right now it is under-insured since the work being done on the car isn't complete ... 50k to 60k (i forget the current amount). once all the work is complete, i will go through the motions to get the agreed value of the 2800cs upwards of 100k to 125k. face it insurance is a form of legalized gambling - you are buying it in case something unexpected happens. but when you need it, you want to be sure that its there. for those of us with 2800cs, it takes a little more work to get it insured for the right value. when i get to that discussion, i will be leveraging the best information i can find on comparable sales of 2800cs.

I’ve had my policy with American Collectors for 18 years now. I had it insured for a stated value of $25k up until last spring, when I noticed the prices the E9s were selling for on BAT. So I called AC and over the phone, with no paperwork, they agreed to increase the agreed to value to $45k, but would go no higher without an appraisal. So I got an appraisal, and AC increased the agreed to value to $79.5k. Of course each increase came with an increased premium rate……

Very nice car I love this red color and orange color also is nice classic color with this car white interior will be real classicJust to chime in here... if others have already said this, forgive me.

Whether it's Hagerty or one of the other collector car insurers, what you want is an "Agreed Value" policy. That is, you want a policy where you say "I want to insure my E9 for $120k" (or whatever your number is), they agree, quote you a price for that, you pay it, and then you have a contract that if the car is stolen or totaled, that's what they'll pay. $120k is a number that Hagerty would NOT agree to for an E9 until a few years ago when one of us wanted that value on his car, they said "we don't think the market supports that," he presented data (mostly numbers from BaT), and they acquiesced. But the point is that if you have a standard policy like you have for a daily driver, if the car gets hit/totaled, you really have very little protection. You can try to justify the value of the car, but they're not really under any legal obligation to pay you what you think it's worth because you haven't entered into a contract with them to pay an "agreed value."

Agreed value policies like the one I have with Hagerty typically have a few requirements:

As someone else said, when I insured my first car with Hagerty (my E9), they raked me over the coals with detailed questions and requests for photos, but every car I buy and add (and there are now 9 on the Hagerty policy) is just a 5-minute phone call. If I buy some ratty 2002 or E28, I call them up, say "Hey, this is Rob Siegel, I bought another car, I have it loaded on the tow platform, and want to insure it before I roll." They say "What value do you want on the car, Mr. Siegel?" I say "Well, right now, not much... $4k." They say "Mr. Siegel, the incremental cost to your current policy will be $16 (or whatever), and when the policy renews, the total additional charge for this car will be $58 (or whatever)." I say "This is the part where I say "I LOVE YOU GUYS!" " (Note that, yes, I write for Hagerty, but I've been a raving fan far longer.)

- You have to show that you and every other licensed driver in the house have another car on which you're listed as the primary driver, and that the car is fully insured. I believe that they leech liability off your other policy.

- You have to show that the car is kept in a locked garage (though I believe Hagerty has relaxed this).

- There is an annual mileage limit in the 2,000 to 3,000 mile range, but it's negotiable.

- But the main thing is that a collector car IS NOT A DAILY DRIVER. You can't use it as a daily. You can't commute to work in it. That's where the cars are at the greatest risk for accidents. You can drive it nights and weekends basically to your heart's content.

I believe I currently have my E9 insured for $60k. It's very pretty, but not at the concours level of some of the other cars on this thread. But these days that's probably a bit low.

For all 9 cars (three 2002s, the Bavaria, the E9, the Euro '79 635CSi, the Z3 and M Coupe, and the '74 Lotus Europa Twin Cam Special), I pay an annual premium of about $1,050. Total. For all nine of them. Of course, I live in the safe confines of Newton MA, and I don't have high agreed values on most of the cars.

--Rob

View attachment 136596

Still to low a valueI’ve had my policy with American Collectors for 18 years now. I had it insured for a stated value of $25k up until last spring, when I noticed the prices the E9s were selling for on BAT. So I called AC and over the phone, with no paperwork, they agreed to increase the agreed to value to $45k, but would go no higher without an appraisal. So I got an appraisal, and AC increased the agreed to value to $79.5k. Of course each increase came with an increased premium rate……